With the recent announcement from Chancellor, Rishi Sunak that the UK card contactless limit will be increased again from £45 to £100 at some point over the course of this year, here is everything you need to know about the pros and cons of the increase and how the banks are planning to support their customers with the new change.

Just a year ago the limit for tap to pay transactions was increased from £30 to £45 to help make card-based payments easier, quicker and with less contact with the payment terminal keypad, throughout the periods of lockdown during the COVID-19 pandemic. Now, the government have announced they are looking to increase this even further, by more than doubling the amount to £100.

Is giving anyone who can get their hand on your bank card the ability to spend up to £300 (the proposed daily limit for contactless spend) perhaps just a step too far - or is this a welcome change to our payment habits?

Why some will love the new £100 limit:

- Coming out of COVID-19, we need to encourage people back to retail stores to help the economy grow. Could the increase encourage people to start spending money within the sectors that really need it such as retail and hospitality, and in turn give a much-needed boost to the economy? When the contactless limit increase from £30 to £45 last year, we saw the average amount spent per each contactless transaction grow to just over £12, which equates to nearly £1 in every £3 spent in the UK according to Barclaycard.

- Contactless fraud only made up 3% of the £288 million lost to credit and debit fraud in 2020.

- Supports the theme of ‘Payment Choice’ – and brings the capabilities of contactless card payments closer to some other forms such as Apple Pay - that currently has no financial cap when you use it to pay for goods. However, digital wallet payments such as this do come with the added security of biometrics i.e., face scanning or fingerprint access, which our credit and debit cards do lack – so extra care of your card will be required.

- Raising the contactless limit might allow consumers in the UK to pay for their average weekly grocery shop (which was noted at around £60 in 2019) with a tap of their card. However, £100 is a vast jump from £60.

Reasons to be cautious:

- With the contactless limit increase, consumers will be even more vulnerable to theft. With a £100 limit, that allows up to £300 per day to be spent using contactless. Money that could then be stolen with just the tap of a card. Even if your bank offers protection against such fraud, you are likely to have your account locked and cards frozen while the matter is resolved – a major inconvenience.

- The introduction of the higher contactless limit could increase how often you need to enter your pin number due to heightened security and your bank asking for pin verification more often.

- Consumer readiness is a factor here as well, with over a third of Britons stating they feel the new limit is too high and could cause issues.

- With an increase in unemployment and debt over the last year, due to COVID, many have found themselves in difficult financial situations or even within debt management plans. Both, which mean relying heavily on budgeting, and the ability to spend £100 without a second thought could be detrimental to their financial situations.

- With contactless still being a relatively new technology to a lot of British people, and something that perhaps is not trusted by the whole of the British public, the announcement has left not only consumers but businesses and banks with divided opinions.

- There is over £8.5 million in loss due to contactless fraud every year.

- A further increase to contactless payments could be yet another push towards a fully digital and cashless society, meaning the UK continue to run the risk of financial exclusion. Cash is still an integral part of many people’s day-to-day across the UK.

'The focus cannot solely be on making things more convenient for those that can benefit from developments in payment technology. Millions of people still rely on cash to pay for essential products and the cash network needs to be protected for them, as the rapid pace of cash machines and bank branch closures shows no sign of slowing down.' - Gareth Shaw, Head of Money at Which?

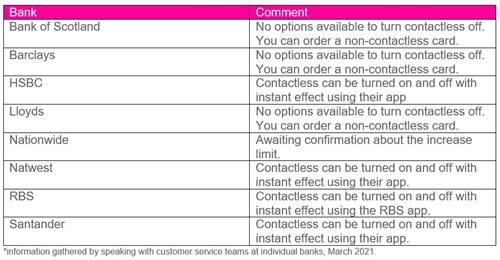

Managing your Contactless Card Limit

After speaking with a number of high street banks, it was clear they have had no confirmation when the increase will happen and if in fact, the increase will happen, however the options for managing your card limit with the main UK banks currently are detailed below:

Many digital banks are responding to the increase by potentially allowing customers options to choose their contactless limit (within the £100 limit) and advising stronger security from the banks, such as more PIN checks is needed.

Meanwhile, the digital bank Starling previously said a few weeks ago that it would 'strongly recommend that a system is introduced where customers have to authenticate higher payments to limit fraud exposure.'

In conclusion, there is no immediate impact, as the increase has not yet been confirmed but before this, there does need to be considerate about the impact and consequences of such a high increase for businesses and consumers alike.

One thing that we need to continue is to ensure that customers will have a choice how they pay, as many do not have the resources, tools, or capabilities to take part in a fully digital world. There has been a number of stories across the news throughout 2020 about customers and businesses suffering due to the card payment only policies, with the most prominent being the Bakery Manager who was fired for using her own card to pay for elderly customers’ purchases, just to allow them to continue paying in cash.

With over third of British people saying they have been turned away and stopped from making a purchase in the last year, due to them having cash only, this doesn’t just impact on the customer but on businesses as well, which are now missing out on selling goods.

Caution and consideration will be required as this proposal is evaluated – and public feedback can be shared.